Physical marketplaces are important cultural artifacts that demonstrate the importance of economic exchange for the pace and improvements of everyday living. And as Rachel Black said in her ethnographic account of Turin’s Porta Palazzo, “What other public spaces still bring together such an important cross-section of a cit’s population? What places allow for open discussion of just about any topic?” (2012, p. 38-39)

This tour can be conducted on foot, but links to virtual resources are also provided.

Portobello Market, W11 1AN

The world’s largest antique market, in the famous Notting Hill. It’s main trading day is Saturday but the area also contains numerous permanent shops. Follow on Instagram to see details of virtual fashion markets on Fridays.

Brick Lane Market, E1 6QR

Containing bric-a-brac as well as fruit and vegetables, Brick Lane market is part of London’s East End and close to the world famous cluster of curry houses. The market is is open on Sundays and can get very busy! For more information see here or here.

Smithfield Market, EC1A 9PS

Smithfield Market is technically called “London Central Markets” and is located in Farringdon. It is one of the largest wholesale meat markets in the world and the site has hosted livestock for over 800 years.

Fun fact: Scottish revolutionary William Wallace, otherwise known as “Braveheart”, was killed at Smithfield in 1305.

Borough Market, SE1 1TL

Borough Market is one of the oldest and largest food markets in London, dating back to the 12th century. The present buildings were built in the 1850s and house an eclectic mix of speciality foods. Open Monday – Saturday.

The London Metal Exchange (LME) originates from 1571, but was formed in 1877 and moved to its current location in 2016. It remains one of the few physical trading floors for a major commodity market – activity is conducted within an open outcry “ring”, which gets its name from when traders would mark out a ring using chalk on a coffeehouse floor. For more on its history see here.

Many consider inequality to be a key social problem, and yet economics is all about delving beyond intuitions. Do we have good data on what has happened to inequality over time? What type of inequality matters? Is there an important trade-off to consider when confronting inequality? The answers to these questions may be controversial, but they are relevant and important.

Imagine trying to answer the following question:

A study by Gimpelson and Treisman (“Misperceiving inequality“, NBER Working Paper 21174) found that:

In 29 of the 40 countries a majority of respondents who ventured a guess guessed wrong.

In 29 countries, the leading choice attracted fewer than 50 percent of those who guessed.

In almost three quarters of countries, most respondents who thought they could identify the general pattern of inequality got it wrong.

“loads of the objections people have to inequality, if there is any truth to them, are probably actually objections to perceptions of inequality, which may be more driven by media coverage than reality. If that’s true, then trying to reduce inequality in fact is a waste of time — you should try to get the media to talk about it less instead”

I think it’s important to recognise that we simply don’t have sufficient wealth for everyone to have a reasonable standard of living. Even if you somehow confiscated the entire global GDP and shared it equally everyone would only get a monthly amount of $1,191 for one year. ($117.2 trillion between 8.3 billion people). This is a reasonable income for many parts of the world, but would lock us in to present consumption power. Would you have wanted your parents to have made a similar trade back in 1985, which would be $12 trillion between 5 billion = $2,400, i.e. less than $7 per day? (I’ve used income, rather than wealth, because the data is better. These figures should also be adjusted for purchasing power, but it’s only meant as a back of the envelope exercise).

Vincent Geloso has challenged some of the work done by Gabriel Zucman. You can read more here:

Thread: Let us be clear — the work of Gabriel Zucman should be taken with a major/huge grain of salt. Largely because he and his colleagues have been sloppy as hell. I will not mince words here and list the litany of sloppiness #econtwitterhttps://t.co/4icOSMcZc7

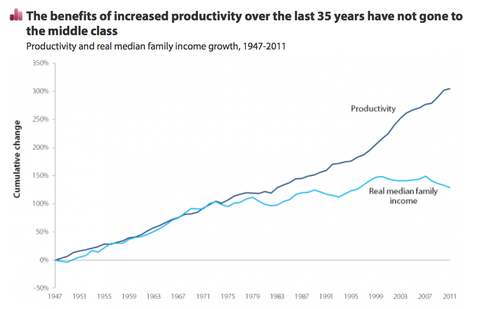

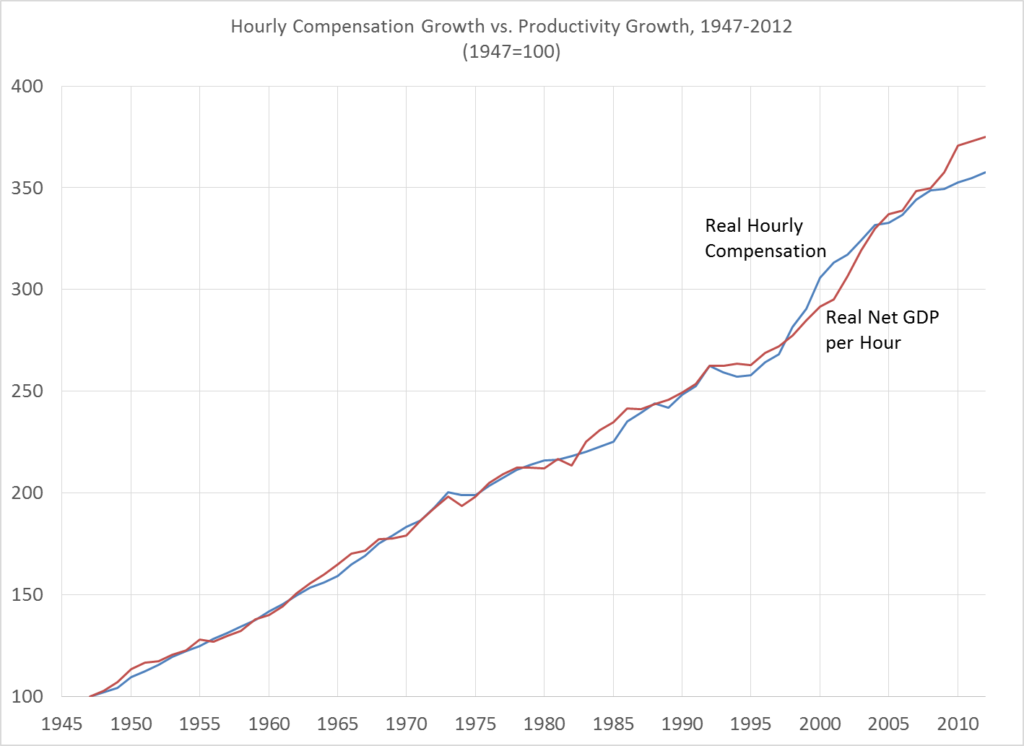

Vincent has also criticised this chart showing the supposed derailment between productivity and wage growth:

According to Scott Winship, “the charts used to demonstrate the supposed breakdown of this relationship obscure the reality that productivity and hourly compensation continue to track each other”. The main problem is that the chart shows family income rather than hourly pay (or, better still, hourly compensation). This chart shows a more like-for-like comparison:

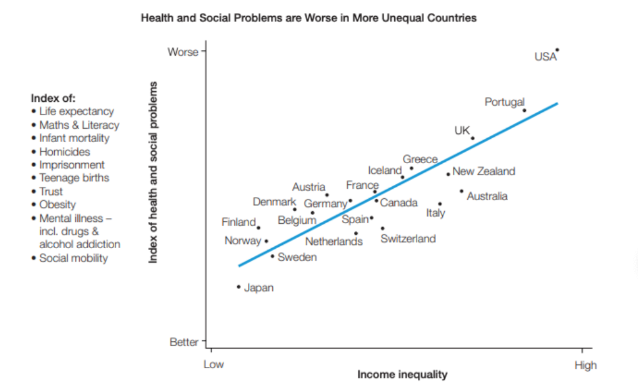

I’ve often seen students link to this graph:

On initial inspection this graph looks highly dubious:

The selection of countries is suspicious (why exclude countries that have more income inequality than the US, and why include Finland but not Singapore?)

The “Index of health and social problems” looks arbitrary and prone to manipulation

However I’ve not been able to find the actual source yet. I assume it comes from ‘The Spirit Level‘, which I believe has been quite firmly debunked:

Snowden, Christopher “The Spirit Level 10 Years On” – When The Spirit Level was released back in 2009 it caught the imagination of the public, by providing empirical evidence to claim that rising inequality was a serious problem. Chris Snowden debunked a lot of the analysis in his book, The Spirit Level Delusion, and this short blog post updates the data to show that not only was the original analysis flawed, but it no longer holds.

Oxfam are also renowned for using dodgy statistics. For example:

Here is an article from Marginal Revolution providing context and assessment of the tribunal that found Next had broken the Equality Act of 2010.

Aside: Sometimes I’m asked what I really think about inequality. Really? That the there is no ethical basis for being concerned about inequality per se. In fact, the best argument to take it seriously is because low educated and xenophobic natives, who have hit the jackpot in where to be born, hold civilised (i.e. cosmopolitan) society to ransom by threatening extremism of various sorts and civil disorder unless their concerns are met. Ideally, we prevent all that from happening by ensuring nominal income stability and productivity growth. But there’s no moral basis for “equalising” arbitrary distributions. Our moral concerns should be focused on eradicating poverty and destitution; and ensuring a competitive market economy that rewards wealth creation and limits rent seeking. If forcing Charles Koch to emigrate improves your metrics of success, then I demur.

My view of the inequality debate is informed by “Fast” Eddie Felson, from ‘The Hustler’.

Luxury

I was very disappointed when Rimowa were sold to LVMH and switched from being a high quality travel company to part of a luxury brand. As Michael Story said,

As per Mary Douglas I view high status consumption goods as part of our need to separate ourselves from others, and signal which groups we belong to. I don’t play those games (at least not on those margina) and think it’s a bit of a waste of resources to do so. But I respect people who admire beauty, design, and the pursuit of aesthetics. Live and let live, I say. But tax the hell out of them.

I largely share Martin Wolf’s (2023, p. 283) criticisms of a universal basic income (UBI) in that by being so intentionally ill targeted it creates too much of a waste of limited public funding – “A UBI at a high enough level to render targeted assistance to those who are vulnerable, needy, and deserving would be unaffordable, while a UBI that is affordable would benefit many people who do not need the money and fail to benefit important services and people who need more than they have now.” I prefer a moderate income tax with generous allowances and incentive compatible welfare payments.

We can think of the state as an “insurer of last resort”, with its access to taxation permitting favourable terms for mitigating risk (p. 274). By being able to compel people it also avoids the “adverse selection” problem that befells individuals in particular need. This helps to explain the main economic justification for a well functioning welfare state (p. 276):

Incomplete private insurance

Incomplete capital markets

Note though that improving the market in those two areas would reduce the need for widespread social protection.

Slavery

For an overview of the debate surrounding the role of slavery in the rise of the West see:

“Claudia Goldin on Inequality“, Conversations with Tyler, Oct 6th 2021 – this conversation focuses on gender inequality and the labour market in particular, and although some of the discussion is aimed at graduate students they pose some excellent questions to reflect on.

“Thomas Piketty on the politics of equality“, Conversations with Tyler, April 20th 2022 – Tyler challenges Piketty on some of the political economy arguments relating to progressivism and does a good job putting Piketty’s work into a history of economic thought perspective.

Ep. 28: Vincent Geloso — Should We Care About Inequality?, The Curious Mind, February 12th 2020 – Vincent talks about which types of inequality are most important to reduce and discusses some of the academic literature that has contributed to our understanding of the issue. His main claim is the need to build a dashboard and avoid overly simplistic explanations or solutions.

“Roland Fryer on Race, Diversity, and Affirmative Action” EconTalk, September 4th 2023 – Fryer explains how the study of discrimination can be approached in three main ways: preference based (e.g. Gary Becker); information based (e.g. Kenneth Arrow); and structural (i.e. sociologists). He summarises his career, talks fondly about the influence of his grandmother, and the importance of combining intuitive wisdom with rigorous data analysis. His main point is that wage discrepancies are not necessarily discrimination, and companies often lack the curiosity or capability to use the data at their disposal to really understand the problems they face. This helps to explain why the benefit of diversity training is zero, and the impact of mandatory diversity training is possibly negative.

Recommended film:

You can see the trailer to Parasite here:

Here are what I consider to be a conventional and alternative take on the movie:

I also recommend the 2021 BBC series Chloe. As this Guardian review demonstrates, when it says “I hope she gets away with everything”, some viewers can actively root for despicable behaviour if it’s presented as a commentary on inequality.

During the class I say that it is inconceivable to have an American movie that portrays wealthy people in a positive light. Potential counter examples include:

The Dark Knight Rises (2012) – the good guy is a billionaire, the police are heroes, and Bane occupies Wall st… I’m not sure the Batman is a positive depiction of wealth, but it’s certainly a very rare example of a movie that is more right wing than left wing.

One Day (2023) – Dexter is obnoxious and his wealth and priviledge is not portrayed in a positive light, but we certainly sympathise with him and, as this Guardian review points out, his “wide-boy charisma and frightful yet endlessly forgivable privilege are perfectly pitched; I forgive him a thousand times. His poshness is neither glossed over nor glamorised; it is simply integral.”. Dexter’s dad is a good man, who we sympathise with, and we don’t hold his wealth against him. That’s something, I guess. (Note this isn’t American, or a movie, but I’m open to anything!)

Saltburn (2023) – this film is a challenging watch but very good (the line “she’d do anything for attention” is perhaps one of the funniest I’ve ever heard). If you’ve read Engleby then I think you lose a large part of its power and originality, and if you understand the Solow growth model you may be confused by the ending. In terms of its implication for inequality, you do sympathise with the rich, and it sort of parallels Parasite’s warning about trust and naivety. But Oliver isn’t poor (despite his bad accent, Prescott is fine!), and the Catton’s aren’t portrayed as having earned their wealth. They are not horrible people but we do laugh at their buffoonery and aren’t asked to respect them. Felix isn’t atrocious but he’s manipulative. Like Parasite, it shows the rich as victims of those less fortunate, and unlike Chloe we’re not supposed to cheer them on. But it doesn’t portray wealthy people in a positive light.

Loot (2022) – I haven’t seen this but the basic premise (I think) is that it is possible to feel sympathy and even affection for a multi-billionaire. And yet, onlyif they become a philanthropist. And also, the husband is the villain.

Finally, if you like the plot device from Parasite, with people appearing from underground captivity, confronting a confusing situation as a result of odd costumes, leading to violence and mayhem… then I recommend Emir Kusturica’s Underground (1995):

Learning Objectives: Survey the latest empirical work on inequality and relate this to wider social issues.

“Stagnation, my dear boy, what is more soul-destroying than stagnation?” C.S. Lewis, The Great Divorce

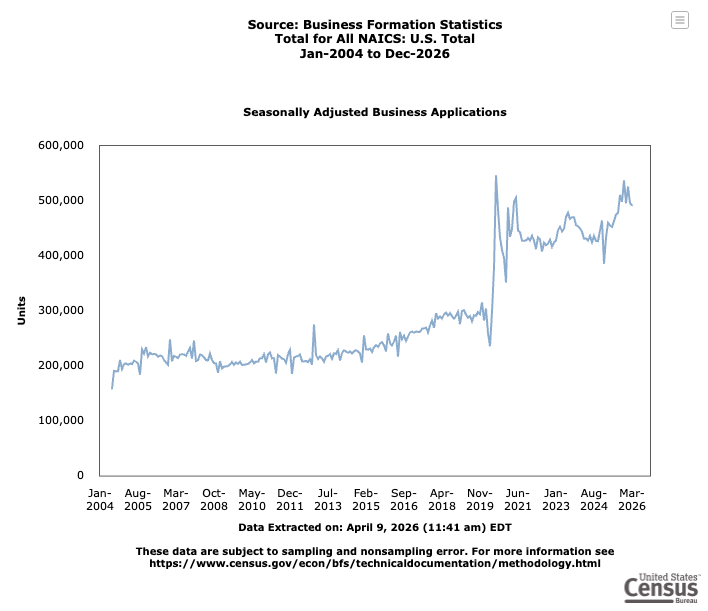

In the lecture I say that “start up rates are falling” but that was from a 2014 paper that I wrote. Data from the US Census Bureau suggests that since then they have been rising.:

According to Max Grossman, as of 2021 half of all scientific papers that had even been published had come in the last 12 years, and yet much less than half of scientific progress had happened in that same period.

Here’s a great image showing a long-term timeline of technology (but notice the gap between smartphones and Now):

Here is a video showing the opening of the Empire State Building:

And don’t forget just how amazing it was when people saw the iPhone for the first time:

For more on whether Jeanne Calment really was the oldest person ever, see Wikipedia. Saul Newman is a demographer who has found that the places that have lots of people living over the age of 100 tend to be riddled by clerical errors and pension fraud – he won an Ig Nobel in 2024. This chart shows that once birth certificates became widely adopted far fewer people claimed to be very old.

Here is The Economist on how claims of people living to a great age decline when birth certificates are introduced.

As Alec Strpp says, “Areas of the world with people claiming to be 110+ years old are actually just places with poor record keeping and a lot of pension fraud.”

Isn’t it weird how you used to be able to easily tell when a TV series was set from the fashion? And yet long running recent shows are much harder to date. For example,

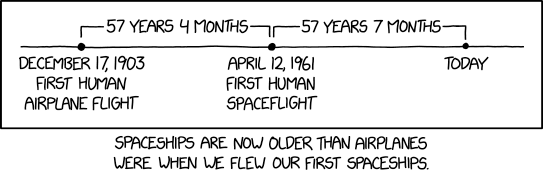

I was saddened to learn recently that same amount of time had passed between the first human airplane flight and the first human spaceflight as between the first spaceflight and 2018 (see here).

Here is a good defense of the importance of aviation:

“It has offered people the opportunity to migrate from one country to another It lets them return home to visit their families. It has provided jobs. Driven innovations in new technologies. It has made our societies more diverse and multicultural and has allowed us to experience the beauty of other countries. these are experience I want everyone in the world to have access to” (Ritchie, 2024, p.99)

To some extent this lecture is about trying to work out what happened in the early 1970s. This website poses the same question: https://wtfhappenedin1971.com/

Some interesting (and possibly related) facts about this period:

The lecture provided some pessimistic views on transformative breakthroughs. But every now and then I notice the power of steady, incremental progress. For example:

Are we running out of ideas? Freakonomics, November 2017 – the key points are to consider whether productivity is happening but isn’t being captured by GDP due to spillovers

Textbook Reading: Chapter 1 (Section 1.2, pp. 16-29)

The purpose of this session is to realise that value comes from satisfying people’s needs, and that this leads to a broad and insightful realisation that:

Competition is when anyone else tries to satisfy the same customer needs that you do.

Innovation is trying to find better ways to satisfy your customers needs.

Entrepreneurship is successful when you understand your customers needs better than they do.

Steve Job’s famous advice was to not listen to your customers. This is in contrast to Tyler Cowen’s “law of interesting content” – which is that interviewers should have the conversation that they want, not what they think their listeners want.

I think it is incorrect to say that the reason diamonds are more valuable than water is because they are scarcer. This would be using the term “scarcity” to refer to a relative amount of present consumption, but that is obtuse. We normally use scarcity as a collective assessment of the availability of a good. In other words, there is no such thing as personal scarcity.

Christensen, C., et al, 2016, “Know Your Customers’ “Jobs to Be Done”” Harvard Business Review – the seminal account of thinking about service provision and how to understand your work from the perspective of your customers.

Learning Objectives: Link a thorough concept of value with implications for competition and innovation. Derive demand curves.

Cutting edge theory: Jobs to be done

Focus on diversity: Economists typically take preferences as given, but we can provide a theory of demand reflecting “the individual’s commitment to an intelligible universe” (p.52), where goods are considered to be a visible reflection of culture. Mary Douglas (1921-2007) was one of the world’s most admired social anthropologists, and her 1979 book, ‘The World of Goods’, provided a rich and compelling illumination of consumption patterns.

New York is the classic metropolis and when you stand in Times Square you feel that you are in the centre of the world.

Most great cities have a similar aspect – the river upon which it originates provides a bearing and context. I love Liverpool in part because the two Mersey tunnels preserve the unique skyline (and provide a clear view of where I got married).

Liverpool – the city of my adoption and my affection

New York – and when I say New York I obviously mean Manhattan – is special because there is no dominant waterfront. The fact that it’s an island makes it inward looking, and instead of being in a city to judge by itself, you feel that you are at the centre of all cities, and therefore all modern civilization.

My first trip to New York was via bus from Washington DC. We were offloaded in Chinatown and it was freezing cold, so we went straight into the nearest diner for coffee and doughnuts. After dumping our bags in the hostel we raced to the Empire State Building and caught the last elevator ride up. What was damp rain at street level was snowfall at the top. Romantic, and majestic.

I call myself a citizen of the world and New York the capital of the world, Jack Reacher (in Gone Tomorrow, p. 16)

My last trip was to present a paper at the Eastern Economic Association annual conference. The keynote was delivered by Ed Glaeser, the world’s leading economist on cities. He is a sharp, dazzling speaker, and watching him perform with a New York City backdrop was a thrill. Satisfying, and triumphant.

The city as the engine for social change and increasing well-being is one of the truly great triumphs of our amazing ability to form social groups and collectively take advantage of economies of scale (West, 2017, p.186).

What I love most about cities is the juxtaposition of energy and possibility and the amount of personal space they provide. An atomised city provides a certain sanctity. Here’s how to spend time alone in NYC.

Cities are the crucible of civilization, the hubs of innovation, the engines of wealth creation and centres of power, the magnets that attract creative individuals, and the stimulant for ideas, growth, and innovation. (West 2017, p.215).

They incubate immense wealth creation by permitting specialisation and market exchange. Consider David Schmitdtz (2023, p. 101):

In a village, a poor man’s son might grow up to be a doctor, but no one will push the frontier of oral surgery. Why not? Because in villages there aren’t enough customers. Specialized trades emerge only where a customer base is large enough to sustain them. To find specialists, we go to a commercial hub such as London. In London, someone who might otherwise be the village carpenter can specialize in crafting violins. Economies of scale make possible fine-grained specialization, thereby fostering new heights of excellence.

I like cities for the same reason that Frank Renzo does, in Sebastian Faulks’ ‘On Green Dolphin Street’,

I like the fact that it’s impersonal. No one troubles you. That’s what cities are for.

The downside of this, of course, is the potential to slip out of life, unnoticed. Cities come with costs.

They are the prime loci of crime, pollution, poverty, disease, and the consumption of energy and resources. Rapid urbanization and accelerating economic development have generated multiple global challenges ranging from climate change and its environmental impacts to incipient crises in food, energy, and water availability, public health, financial markets, and the global economy (West 2017, p.215).

But surely we can agree that the solutions to these modern problems must include (i) energy efficiency; and (ii) wealth. Thus cities are crucial.

Of course most cities develop along trading routes, and the best cities are historic ports.

“In port cities, arts proliferate and people innovate because ports are hubs or commerce; they are where cultures meet” (David Schmidtz, 2023, p. 101)

Each trip to New York is a combination of revisiting favourite eateries and seeking new ones.

Sombrero – When you come from the UK, and the alternative is a chain such as Tortilla or Chiquito, it’s nice to sit in a Mexican restaurant, with a wide range of tequilas, and full plates of decent fare. Of course there are better options in New York, but I’m 5 mins from Times Square and I get: (i) Flat (ii) Corn (iii)Tacos with a small bowl of rice and refried beans. My main motivation for my first visit was the proximity to my hotel, but I’ve come back several times since.

Xi’an famous noodles – I vouch for the Spicy Cumin Lamb burger, but there’s a lovely depth of heat and lip tingling joy across the menu.

To try:

Pisillo Italian Panini – the first sub that I had in NYC blew me away. Multiple meats, and it required a dislocated jaw to bite into! For a wide choice of Italian style subs, this is the place

The Turnmill – this is the official bar of the Everton FC NYC supporters club. What’s better than a packed pub in a foreign city, on a matchday, covered in TVs, full of fellow fans? Savour the crisp walk of anticipation from the subway ready to sink a cold pint at 10am. Bizarre, but worth doing.

Take a ferry from pier 11 to Dumbo, visit the Time Out Market (in particulate take the lift up to the bar for a view across the terrace) and then walk back across the Brooklyn Bridge

I’m not sure when I’ll next go back to NYC. But I miss it.

I don’t play poker but I have a couple of friends that do. I recently asked them what resources they’d recommend for people wanting to get into it, and thought I’d share their advice.

MIT has a video series called “How to win at Texas Hold ‘Em”:

Depending on the type of game you wish to play, further resources may be more relevant. The best forum, and one used by many of the top professionals to discuss play is 2p2: www.twoplustwo.com.

Some excellent beginner’s resources are available at Upswingpoker.com

Poker player Annie Duke uses the representative heuristic to her advantage. She often encounters opponents who make assumptions about her ability because she is a woman. She categorized her male opponents into three groups, based on how they treated her – the flirting chauvinist (who she’d be nice to, and distract); the disrespectful chauvinist (who underestimated her, so she’d be able to bluff); and the angry chauvinist (who would do anything to avoid being beaten by a women, so her response was to be patient and wait for them to become reckless).

The scenario method is a useful, creative, and increasingly popular way for managers to reframe their perspective and improve their organisational resilience. The course shows how to recognise the driving forces that will affect the future business context and consider the present-day implications. By building detailed and imaginative narratives, participants will learn how to confront uncertainty and become more confident in conditions of change. The lecture content contains the cutting-edge practice of the scenario method and the blended approach permits flexibility, agility, and collaborative project work.

Oxford Scenarios Programme, Webinar, September 2017 – this provides an excellent overview of two fascinating case studies: Rolls Royce and the Royal Society of Chemistry.

For my report on SMRs see here. For my analysis of the situation in Belarus see here.

To learn more about Everton’s relegation battles and their link to scenario planning, see these two articles:

It summarises intelligence success and failures and quotes a German official: “The main thing we took away from all of this was that we need to work with worst-case scenarios much more than we did before.” It concludes, “For many, the key intelligence lesson from Ukraine was stark: do not rule things out, just because they might once have seemed impossible.” Indeed, the Canadian military are now modeling an American invasion.

In 1997 Wired published an article called “The Long Boom” in which Peter Schwartz and Peter Leyden provided a “history of the future 1980-2020”. You can read it here.

If you want a great example of how to build an engaging future reality, l highly recommend: Children of Men (2006).

Learning Objectives: Build and use scenarios. Think creatively about alternate futures. Link scenario planning to strategic issues.

Why is the scenario method so important? Because, as Adam Martin mentioned in his interview with Peter Boettke, in economics the emphasis on choice is because we live in a world of scarcity. The conditions of uncertainty, however, also means that we require imagination. Scarcity and uncertainty are the context. Choice and imagination are the consequence.

The training scene from Rocky IV demonstrates the difference between the USSR (technologically sophisticated but lacking in heart) and the US (backward but free).

The 2023 Christmas edition of The Economist included a fascinating account of extended market order, economic development, and the role of capitalism in Indonesia:

What should Widodo do? Indonesia is a large, populous middle-income country. It faces no major near-term security threats. It has a small manufacturing base and no major non-commodity export sectors. What is the best non-bureaucratic 10 page economic development briefing document and set of prescriptions that one could write for Indonesia’s president?

Here’s my analysis of Belarus, using many complementary concepts.

As

As

Course introduction

Course introduction