NGDP masterclass

This webpage gathers some key resources to help you understand what a NGDP target is, and why I think central banks should be more open to adopting them. I am convinced that delivering macroeconomic stability should be the prime objective of any central bank, and that an NGDP target would be a good way to achieve this. Let’s see why…

What is an NGDP target?

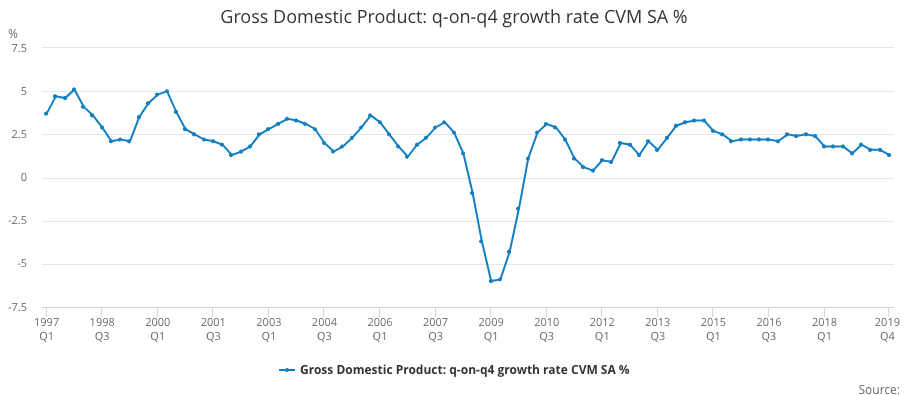

You probably know that GDP stands for Gross Domestic Product. This is the conventional way of measuring economic activity, and reveals the market value of final goods. When we’re interested in whether people are getting richer or poorer, we look at real GDP, which strips out the effects of inflation. This allows us to make meaningful comparisons about the productive performance of an economy across different time periods, and the chart below shows what’s happened to GDP in the UK from 1997-2019:

Source: ONS (Gross Domestic Product: q-on-q4 growth rate CVM SA % (IHYR))

The real growth rate for the UK from 1949-2019 averaged 2.5%, but more recently it seems to be below this. While this may be a concern, in normal times it is driven by factors outside the control of central banks (such as the productivity of labour and capital).

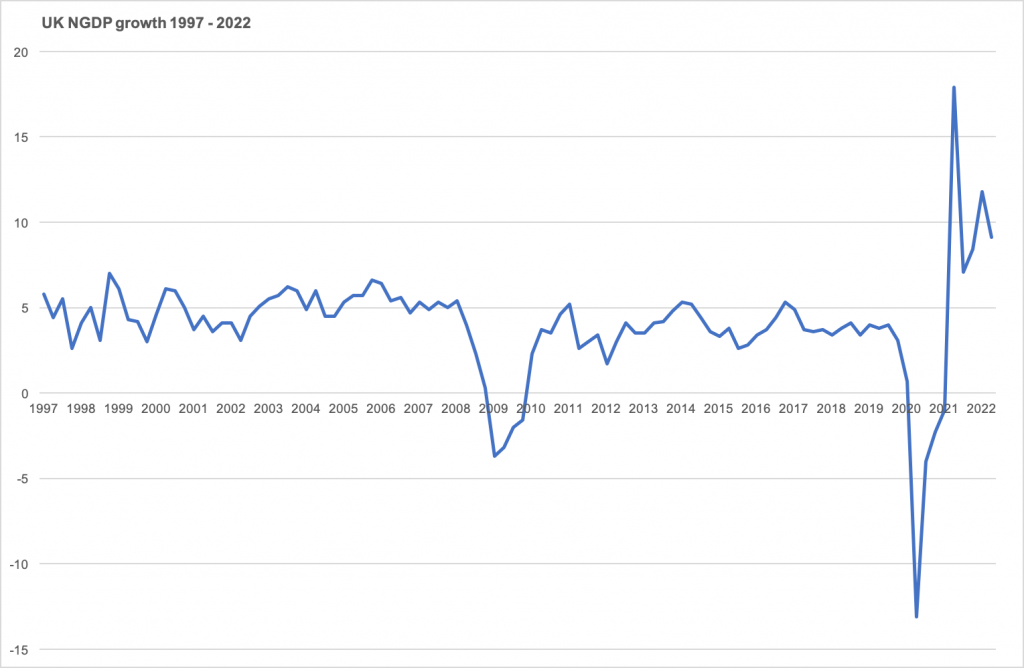

Central banks do, however, have a large influence over the nominal growth rate, which is the cash value of economic activity (i.e. without stripping out the effects of inflation). The chart below shows annual NGDP growth from 1997-2022.

Source: ONS (Gross Domestic Product: q-on-q4 growth quarter growth: CP SA % (IHYO))

Notice a few interesting things:

- Prior to the global financial crisis (i.e. from 1997-2008) it was fairly stable at around 5%.

- It significantly contracted during the global financial crisis.

- From 2011-2019 it was slightly more volatile and a slightly lower rate (averaging below 4%).

- It was extremely volatile during the covid pandemic and recent energy shocks.

Now, here are the big claims I wish to make:

(i) The reason that economic performance was reasonably good from 1997-2008 was because NGDP growth was stable.

(ii) The subsequent and more recent poor performance was due to having left that 5% growth path.

What do central banks do?

Most central banks utilise an inflation target, where their primary objective is to deliver low and stable inflation. And this is how we typically judge whether they are doing their job. For example,

- The Bank of England has an explicit 2% inflation target.

- The European Central Bank is supposed to deliver “price stability”, which they believe is “best maintained by aiming for 2% inflation over the medium term”.

- The Federal Reserve has a “dual mandate”, which is a twin objective of delivering maximum employment and stable prices.

However, many economists question whether this is the best way to conduct monetary policy. Instead of trying to keep consumer prices stable and assume that other important variables will follow from that, an NGDP target aims for a stable environment for all wage and debt contracts, because labour and credit markets are more important for economic planning than a specific set of consumer prices. Indeed, NGDP is less volatile than CPI, and NGDP is more relevant for concerns about debt sustainability.

It is therefore interesting to see that even back in 2012 NGDP targets were receiving attention from important central bankers:

- The former governor of the Bank of England, Mark Carney (see here)

- The former chair of the Federal Reserve, Janet Yellen (this speech has been widely interpreted to incorporate attention to NGDP growth in policy decisions)

Some theory

Consider the following “equation of exchange” (where each variable refers to a growth rate):

M+V=P+Y

The power of this equation is that it rests on a tautology, which is that the total spending across the entire economy must be equal to total receipts. That being the case, we can break down total spending into two components: the amount of money that is available to spend (M), and people’s desire to spend the money already in circulation (V). Spending rises when more money gets created, or if people choose to spend more of what they already have. Central banks therefore stimulate the economy either by Quantitative Easing (more M) or reducing interest rates (more V). This “total spending” is sometimes referred to as aggregate demand, but notice that it is equal to the combined rate of inflation (P) and real GDP growth (Y). It is through their ability to determine the amount of aggregate demand that central banks will directly affect nominal GDP (P+Y). And since one person’s expenditure is another’s income, another term for NGDP is nominal income.

For more on using this equation as a foundation for understanding macroeconomic policy objectives and performance, see here.

Some history

Nominal income targets first became popular in the 1980s, when the prevailing focus was targeting the money supply (as pointed out in this presentation by Jeff Frankel). Some big name economists gave them attention, including in the following famous articles: (for a longer list see here)

- Meade, J. 1978, “The Meaning of “Internal Balance” The Economic Journal, 88(351), 423–435.

- Tobin, J., 1980, “Stabilization Policy Ten Years After” Brookings Paper on Economic Activity, 11, 19-90.

- Bean, C. R. 1983, “Targeting Nominal Income: An Appraisal” The Economic Journal, 93(372), 806–819.

More recently, following the global financial crisis, there has been a second wave of interest in NGDP targets, for example:

- Woodford, 2012, “Methods of Policy Accommodation at the Interest-Rate Lower Bound“

- Frankel, J., 2013 “Nominal-GDP targets, without losing the inflation anchor” in Is Inflation Targeting Dead? Central Banking After the Crisis, VoxEU

- Sumner, S. 2014, “Nominal GDP Targeting: A Simple Rule to Improve Fed Performance.” Cato Journal 34 (2): 315–37

- Beckworth, D., and Hendrickson, J. R., 2016, “Nominal GDP Targeting and the Taylor Rule on an Even Playing Field.” Mercatus Working Paper. Arlington, Va.: Mercatus Center at George Mason University (October).

This second wave has come in the context of perceived failures of inflation targets.

We can therefore witness a steady evolution in thought: perhaps instead of being bound by a money growth rule (M), or an inflation target (P), the central bank should instead target nominal income (P+Y). This means that real productivity will determine the split between inflation and real growth – if productivity is strong then inflation will be low, but when there’s a real business cycle slow down inflation is permitted to rise. These adjustments will take place such that NGDP remains stable. This video by MoneyWeek does a nice job explaining how this balancing act is already part of the Fed’s perview:

The increased influence of NGDP…

Scott Sumner has been described by The Atlantic as “the blogger who saved the economy” due to the influence he had over the Fed’s late 2012 QE3 program. You can see a great overview of the rise of Sumner here:

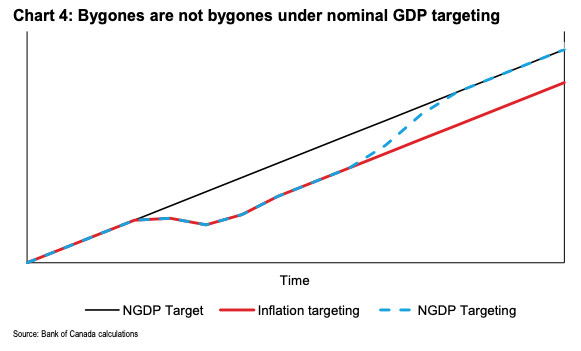

A key thing that he emphasises is that it’s not just the fact the nominal income is a more important variable for macro stability than price stability, but that the expected growth path of a variable is more important than a rate. In other words, if a central bank “misses” a 2% target the question is whether it tries to get back to 2% and consider that enough, or whether they try to get back to where things would have been had the 2% growth path continued. In technical terms NGDP advocates want a level target and, as Mark Carney’s chart below shows, to not let bygones be bygones.

(Astute readers will point out that you could have an inflation level target and achieve the same result, which is indeed the case. But for simplicity we compare the status quo inflation growth rate target and the potential NGDP level target).

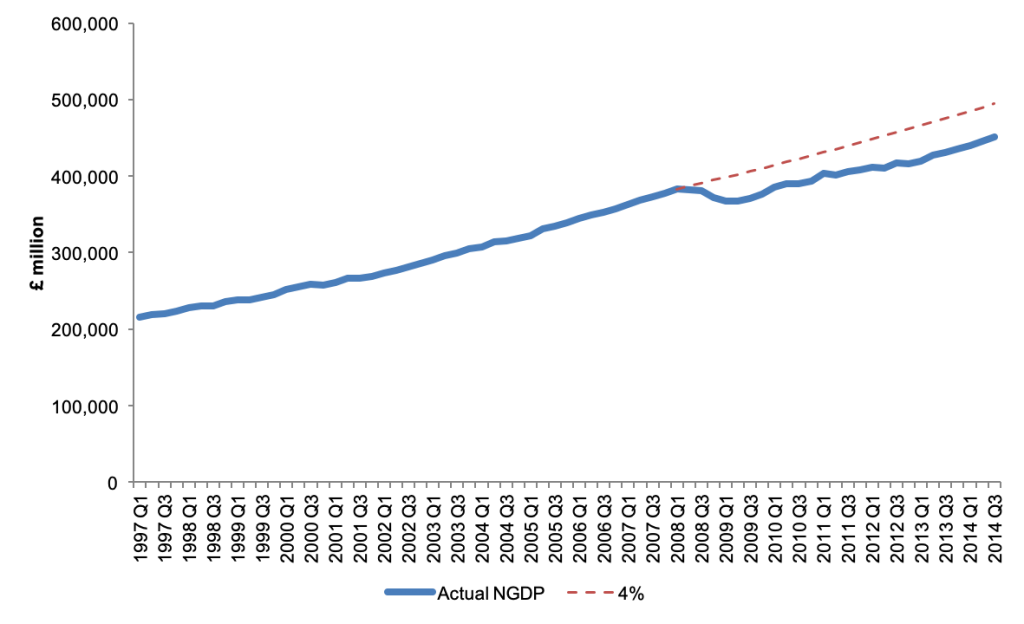

So even though thinking in growth rates is easier to communicate, the power of an NGDP level target is best shown when we look at absolute units. And as the chart below shows the UK deviated from a hypothetical 4% growth path and failed to catch back up again. That NGDP gap represents a permanent loss of economic activity relative to the public’s prior expectations, and forces an unnecessary and painful slowdown.

Source: ONS, own calculations

NGDP targets: pros and cons

We shouldn’t expect a perfect tool for managing the economy, so in this section I want to summarise what I consider to be the three strongest reasons in favour of NGDP targets, and also the three strongest arguments against.

Three good reasons in favour:

- They are good at dealing with supply shocks. An inflation target fails to reflect the reasons for inflation to either be above or below target, and therefore send dangerous signals to policymakers. If inflation is low because of a lack of demand, we need central banks to step in. But if inflation is low because of productivity improvements, then increased purchasing power is exactly what we want. Similarly, if too much aggregate demand is causing higher prices we want central banks to cool things down. But if a negative real shock is prompting prices to spike, the last thing we want is reduced spending, which which compound the negative economic activity. By asking central bankers to “see through” temporary inflation we’re expecting them to be able to make a judgment about the source of inflation. An NGDP target avoids having to do this – by keeping nominal income stable you let the price level adjust automatically to changes in productivity.

- They promote financial stability. A big macroeconomic danger is that when debt burdens become unmanageable this tends to affect wide parts of the economy and has negative knock on effects. A NGDP target means that in a recession inflation will increase and this will erode some of the real value of those debt burdens. People tend to borrow a nominal amount, and inflation means that you pay back less, in real terms, than you otherwise would. This eases the consequences of high debt burdens.

- They promote monetary neutrality. If V is people’s desire to spend money then we can recognise that it is the inverse of people’s desire to hold money, i.e. the demand for money. Like any market, equilibrium occurs when the demand and supply are able to adjust, and when it comes to money we want supply to adjust to changes in demand. Monetary equilibrium is therefore a consequence of NGDP stability. This also will keep interest rates at their “natural” rate, which is when the demand and supply of loanable funds is equal. Rather than using monetary policy to deliver an arbitrary inflation target, an NGDP target approximates a much more important macroeconomic objective: neutrality. It provides a platform where demand and supply interact, providing a stable and meaningful context for economic activity to take place.

Three good reasons against:

- National income data isn’t ready yet. Reasonably accurate estimates of CPI are released every month. GDP by contrast tends to be available each quarter and subject to large revisions. Indeed some people argue that policy mistakes in 2008 were more due to the fact that GDP data was faulty rather than a blind commitment to an inflation target. But even if we had quicker estimates of GDP this isn’t necessarily what we should be focused on. Not all economic transactions are captured in GDP figures, which is a sort of middle ground between a measure of pure consumption of final goods (i.e. no capital goods at all) and the entire capital stock. It serves a useful purpose, but is hardly an accurate measure of what we actually care about. Some would argue that the “correct” form of the equation of exchange is M+V=P+T, where T refers to all economic transactions. But if we include financial transactions in our analysis, the real economy becomes virtually irrelevant. So perhaps a focus on payments data or “average weekly earnings” may be better suited to our objectives than GDP.

- It will lead to greater inflation volatility. By switching to a NGDP target policymakers will be less inclined to ensure a stable rate of inflation. It’s debatable how successful they have been at delivering a low, moderate rate of inflation, but less focus on this may well reduce performance even more. Especially since Y* is subject to change, the choice of NGDP target will lead to quite high variations in inflation. There will also be some confusion amongst the general public, because at the moment we use CPI as our standard measure. However the “P” in M+V=P+Y is not best measured by a basket of consumer goods, it should be the inflation rate that affects the component parts of our GDP calculation. This is referred to the “GDP deflator”. It has taken central banks many years to generate credibility around their ability to get the general public to expect 2% inflation. Switching to a more volatile outcome of a different measure might be hard to explain.

- Not all economies are suitable. An NGDP target is best suited to larger economies, because smaller ones (especially if their are open to trade) are likely to be reliant on particular commodities. For example, for small open economies (in especially those that are commodity exporters) if oil prices rise you would need to shrink the rest of the economy.

Working on NGDP targets

In May 2013 I organised a conference in Copenhagen, hosted by Danske Bank. It involved Lars Christensen as well as Sam Bowman and Ben Southwood from the Adam Smith Institute. Lars coined the term “Market Monetarism” and became known as an early and influential advocate via his famous blog, “The Market Monetarist“. Sam advocated an NGDP target in a letter published by the Financial Times in 2014. And here is a nice video of Ben Southwood explaining how a NGDP target would mean that central banks don’t have to try to work out which shocks to respond to and which to ignore:

Also around this time, in 2016, the ASI published my policy report, Sound Money, which contained an NGDP proposal for the UK.

Some of the key questions to address when considering an NGDP target are as follows:

- Should it be a growth rate target or a level target?

- Should it be set at a high rate (which gives monetary policy more room to manoeuvre, and requires less of an adjustment from nominal wages in a downturn) or a lower rate (which permits mild deflation when productivity is high, and has less distortions on non-indexed factors such as taxes on capital)?

- Should it focus on GDP or some other measure of economic activity such as transactions, or something like Average Weekly Earnings?

- Should it focus on GDP/T/AWE as whole or adjusted for population growth (i.e. on a per capita basis)?

Considering all of these factors, I advocated a 2% average growth in NGDP expectations over a 5 year rolling period. The mains reasons were:

- It retains the public’s understanding of real GDP and inflation in terms of growth rates, not levels

- 5 years is a long enough time period to be a de facto level target

- 5 years is a short enough period to fit into the political cycle (and therefore generate some short term accountability)

- A 2% rate hedges against central bank incompetence at the zero lower bound

- A 2% rate provides a small cushion against deflation (which rightly or wrongly is politically dangerous)

- A 2% rate is low enough to permits a mild deflation whenever productivity grows above 2%

- It avoids the need (for now) to set up complicated futures market

My proposal was trying to strike a balance between those who advocate that total spending is stable (i.e. a 0% growth target) and those who take the current inflation target (2%) and the typical long term real growth rate (~2%) to create a 4% NGDP target. But this idea didn’t catch on, and in hindsight it’s probably better to go for one or the other. Regardless, I was delighted to see that the proposals received extensive media coverage:

It’s more than just a NGDP target

My ASI proposal discussed NGDP targets within the context of wider reforms. I viewed an NGDP target as a step in the right direction away from arbitrary and discretionary monetary policy decisions, and toward a more automated, rule-based system. Some important additional elements relating to implementation included:

- It places a focus on monetary base (which, ultimately, is all that the CB controls)

- It makes open market operations (OMO) the routine monetary policy tool (rather than interest rates)

- It can strip away a lot of distortionary CB activity

- It uses forecasts and market expectations (possibly through futures contracts) rather than historic data

- It can be tied to some automatic mechanism, become a rule, and eliminates discretion entirely

More recently

In June 2020 I participated in a webinar, hosted by the Adam Smith Institute, about NGDP targeting. I wouldn’t expect you to watch the entire recording, but it was a real thrill to share a panel with Scott Sumner.

In September 2021 Scott Sumner was interviewed by Larry White for the Mercatus Center podcast. I recommend the whole episode, but what I found most interesting was Scott’s optimistic take on the influence of NGDP targets. He made a few key points:

-

A flexible average inflation target is one way to permit NGDP playing a role without the embarrassment of abandoning an inflation target.

-

The Fed’s decision to cut interest rates in 2019, despite inflation being high, indicates an increased concern for market expectations (see falling inflation expectations here) and therefore a triumph of market monetarism. (Indeed market monetarists have been credited with having directly influenced the Fed’s decision to adopt average inflation targeting and use market forecasts when cutting interest rates in 2019).

-

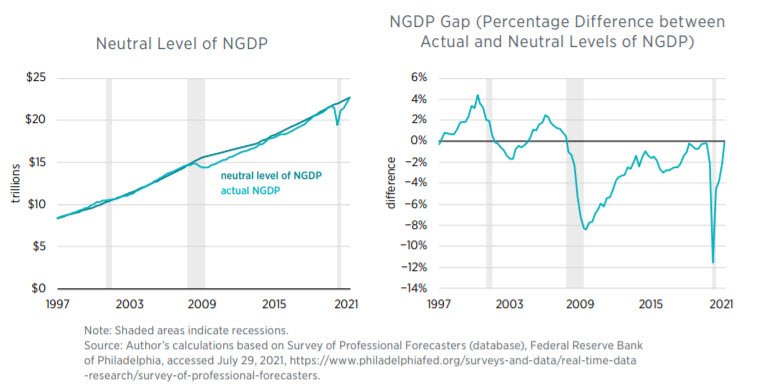

We’ve now got back to the pre-covid NGDP trendline (see David Beckworth’s charts, shown below) which is why this recession hasn’t prompted a debt crisis.

I don’t think this final point is appreciated enough – we’ve experienced a historically unprecedented collapse in economic activity and yet this didn’t have an immediate, obvious, and cataclysmic effect on the banking system, the housing market, unemployment, or corporate or personal bankruptcy levels. Had central banks repeated the mistake of 2008, and allowed NGDP growth expectations to fall, then the consequences would have been horrific. But they heeded the lesson, and reassured markets that NGDP would soon return to the previous trend path.

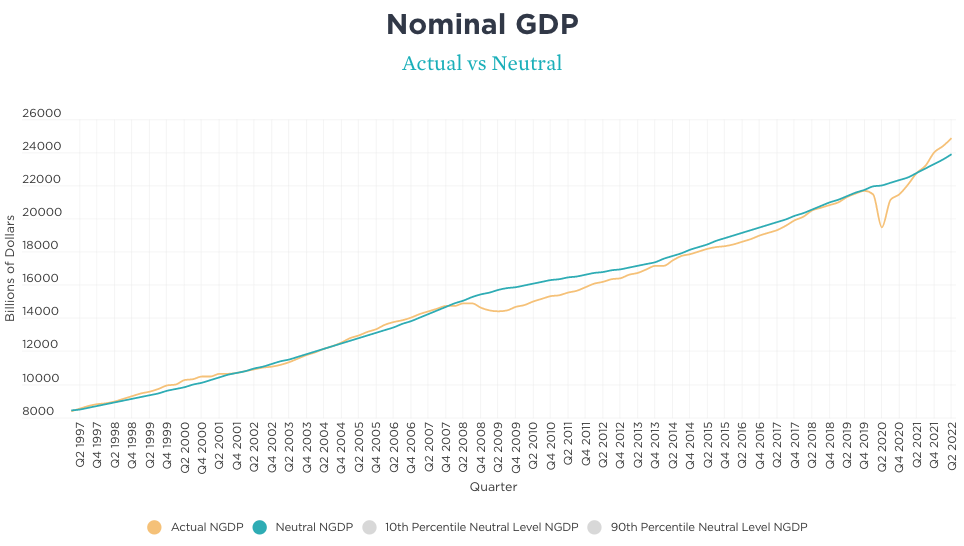

That said, if we look at the figures for 2022 we can see that according to David Beckworth’s excellent data set actual NGDP is now exceeding the amount it would be in order to be neutral. This suggests that the Fed are providing too much support, risking higher inflation and financial exuberance.

Source: David Beckworth. https://www.mercatus.org/publications/monetary-policy/measuring-monetary-policy-ngdp-gap

Whether or not central banks adopt an explicit NGDP target this data is playing a crucial role in our attempt to assess and inform policy decisions. I’m proud to have contributed to this research agenda.

Further recommendations:

Podcasts:

- Lawrence White & Scott Sumner on “The Money Illusion”, FA Hayek Program podcast, September 2021

- The Fed Framework Review, Macro Musings, January 2025 – this is an edited collection of past shows that discussed NGDP targets.

Recommended video:

- What can asset prices tell us about the great recession? Scott Sumner, February 2011 – a great way to see how Scott’s interpretation of events during the financial crisis were seen as idiosyncratic, but now look highly prescient.

- The Role of the Fed, December 2012 – David Beckworth and Scott Sumber present a congressional testimony about market monetarism.

- What does nominal GDP entail? IEA, August 2016 – a short interview with Scott Sumner about how expectations relating to nominal income grwoth are an important tool for central banks when interest rates are low.

️ Relevant newspaper opinion:

- “The Simplest Way to Improve Monetary Policy” by Clive Crook, Bloomberg, April 8th 2022

Relevant academic articles:

- Frankel, J., 2019, “Should the Fed be constrained?” Cato Journal, 39(2): 461-470

✍️ Other things I’ve written

- Did the NGDP crowd win the battle of ideas? Kaleidic Economics, December 27th 2021

- Understanding NGDP targeting Kaleidic Economics, June 24th 2020

- Sound Money, An Austrian proposal for free banking, NGDP targets, and OMO reforms, Adam Smith Institute, 2016

Useful data:

- Mercatus Center Data Visualisation: The NGDP Gap, by David Beckworth

- US NGDP, FRED

- UK NGDP, ONS

️ White paper

- I have written a white paper called “Delivering nominal stability” which is available on request