I am an academic not an entrepreneur, but if there’s one area that I think is ripe for a successful venture it’s creating the go to prediction market. By the early 2000s we had established that prediction markets were an effective tool for corporate management, and we also learnt how useful they could be for a broad range of policy issues. It’s a scandal that governments – and the US in particular – have been so opposed to their use. (The reason is that they’re treated either as gambling firms or futures traders which are two of the most targeted and heavily regulated and industries). According to Scott Alexander:

There ought to be a billion dollar prediction market, maybe a ten billion dollar one. Smart VCs clearly believe something like this, or Kalshi wouldn’t have gotten $30 million+ in investment. Sometimes people who incorrectly believe I know things about prediction markets ask me if know the missing secret sauce. I don’t think there’s any secret. A prediction market will strike it big when it gets three things right at the same time:

Real money

Easy to use

Easy to create your own subsidized markets

It’s a dream of mine that I may have students who manage to put those things together, solve the regulatory issues, and launch a killer app. So far the closest is probably Polymarket but also see Kalshi and Prediki. Here is a website that aggregates prediction market data:

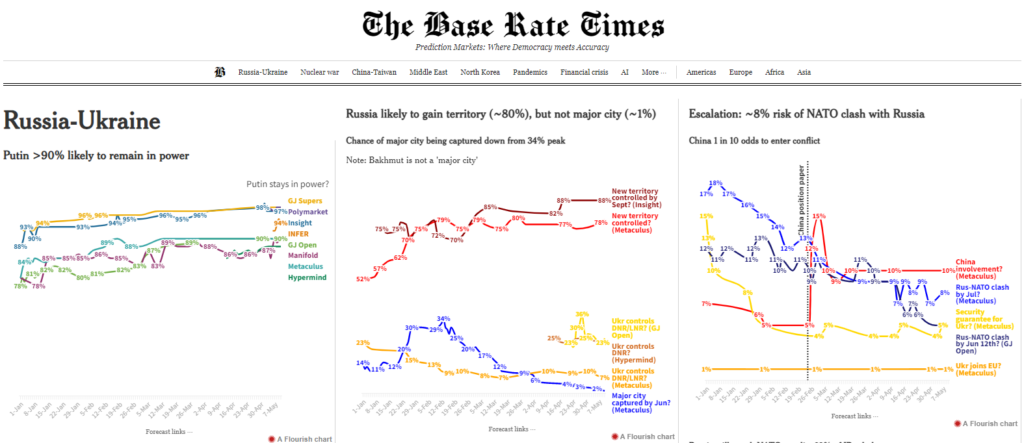

That said, Michael Story is a superforecaster and has made some important criticisms of prediction markets. See here. In his thoughts on the 2024 US Presidential election, Martin Sandbu argues that:

“A nearly 50-50 “prediction” says nothing at all — or nothing more than “we don’t know anything” about who will win in language pretending to say the opposite.”

The following seems to be a really important point:

“For something to count as a prediction, it has to be falsifiable, and probability distributions can’t be falsified by a single event.”

Perhaps the best attempt to explain the failure of predictions markets to gain traction is here:

They define prediction markets as “contracts that trade on the outcome of future events” and split traders into three types:

Savers: people who want to increase their wealth

Gamblers: people who want excitement

Sharps: people who attempt to profit from better quality analysis

They argue that “most things we might want to know about the future aren’t much fun to bet on”, and this results in a lack of demand: “without savers or gamblers to add volume to the market, the market cannot attract enough sharps to create the liquidity to drive prices toward accuracy.” I am not so pessimistic about the potential for prediction markets, but recognise that in order to work they must:

Have short time horizons

Be as fun as possible

Be subsidised

Here are a couple of op-eds on the benefits of insider trading:

Here is a New York Post article explaining how Nancy Pelosi (and her husband) have benefitted from trading off the stocks of companies that she regulates, and why she is resisting efforts to stop Congressional lawmakers from being able to continue to do so. You can track her trades here. Here is a funny halloween costume.

To read more about the “Policy Analysis Market” (PAM) which was designed by Robin Hanson as a tool for the US Department of Defense, but got cancelled in July 29th 2003 having been described as a “terrorism futures market” by the Washington Post, see:

Key technology = fire doors, sprinklers, and alarms that anyone can set off. Imagine how many major hotel fires would occur if staff had to wait to inform senior management before receiving authorisation to call the fire brigade.

Learning Objectives: Understand how to operate a prediction market.

I find it a real shame that for many years I’ve been opening students eyes to the economic benefits of utilising internal pricing between different business units, but almost all attention to “transfer pricing” in the last 10 years or so is in terms of tax avoidance (and therefore something to be discouraged). In terms of useful cases, the most relevant ones from HBR are allprettyold, although Knowledge at Wharton have an interview that covers IBM’s utilisation of transfer pricing.

“Somebody a long time ago invented that metric… [and] they had a reason why they chose that… but that metric is the proxy… And then fast forward 5 years… and a kind of inertia can set in, and you forget the truth behind why you were watching that metric in the first place, and the world shifts a little, and now that proxy isn’t as valuable as it used to be, or it’s missing something, and you have to be on alert for that and know ‘I don’t really care about this metric.. and this metric is only worth putting energy into, and following and improving and scrutinizing only in so much as it actually affects [what I care about]’. [You have to be on guard against] managing metrics that you don’t really understand, you don’t know why they exist, and the world may have shifted out from under them a little and the metrics are no longer as relevant as they were.”

Learning Objectives: Think creatively about how to use markets within organisations

In “What toffs and plebs share“, Ed West uses the signalling vs. counter signalling distinction to argue that institutions such as horse racing or the army demonstrate a unity of peasant culture and aristocracy. He identifies a U-curve of social patterns, with those in the middle trying hard to distinguish themselves from those below, even though this reduces their ability to mix with those at the top.

A good book (that I haven’t read yet) that uncovers how deeply social status affects human action, see:

Textbook Reading: Chapter 3 (Section 3.4; pp. 90-96)

Instructor resource:

“Lemons Buyer”, February 2012

“Lemons Seller”, February 2012

If you are a bit daunted by an academic article, George Akerlof wrote a very interesting essay on how he came up with the ideas and the process of working on the topic. You can read it at the Nobel site.

The lesson for economic policy in a world of intangibles is to invest in “knowledge infrastructure”, i.e.

Education

ICT

Urban planning

Public science

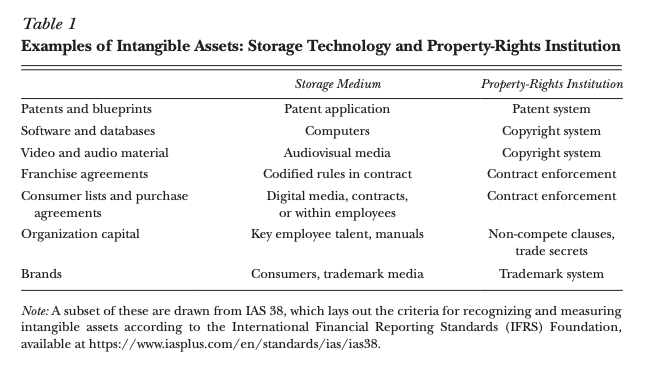

For a nice attempt to avoid treating intangibles as a residual, or less clear category and a meaningful attempt to conceptualise and study them see:

Crouzet, Nicolas, Janice C. Eberly, Andrea L. Eisfeldt, and Dimitris Papanikolaou. 2022.“The Economics of Intangible Capital.”Journal of Economic Perspectives, 36 (3): 29-52.

They argue that intangibles require a storage medium, where “The medium can be a piece of physical capital, like a computer (for software), or a document (for a patent or a design), or a person (for a method or an innovation).” This need for a storage medium implies two things:

Non-rivalry in use

Limited excludability

They argue that, “the extent to which these properties generate a valuable intangible asset— which motivates investment—depends on the properties of the storage technology, and the resulting non-rivalry and excludability, and the institutions that enforce property rights.”

The entrepreneurial state

Some people, such as Mariana Mazzacuto, argue that states should be bolder about their role in technological innovation, and that ‘directed planning’ can improve on market outcomes. Here key work is:

Mazzucato, M. (2013). The entrepreneurial state. London: Anthem Press.

“she ignores the opportunity costs of the spending she claims was partly responsible for innovation and growth”

[she] “fails to recognise that those elements of public spending that may have generated benefits were not ‘planned’.” (Indeed they “appear to have been unintended or accidental consequences emerging from essentially random spending in the defence sector”).

In conclusion, “the Mazzucato case for state-based experimentation… is the suggestion that if governments commit to spending enough public money on their favoured projects it would be remarkable if none of this expenditure did any good. Yet, this position hardly amounts to an endorsement of the transformational potential of the state.”

Microclimate

When talking about macroeconomics I think it’s important to distinguish between the overall economy and the circumstances of an individual firm. We can’t always assume that macro conditions are felt the same by each company within it. I explain more in this video:

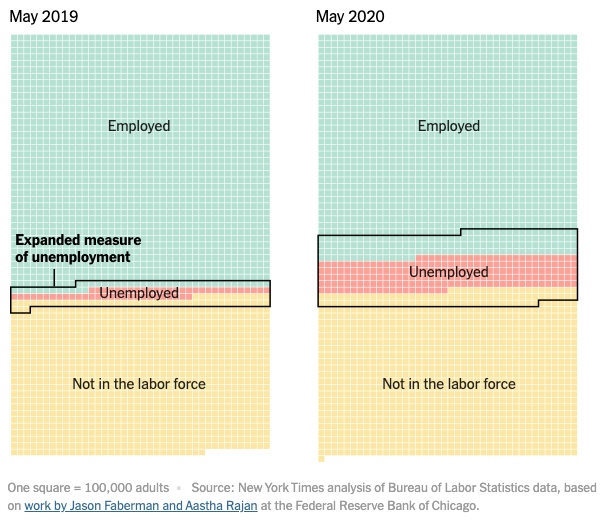

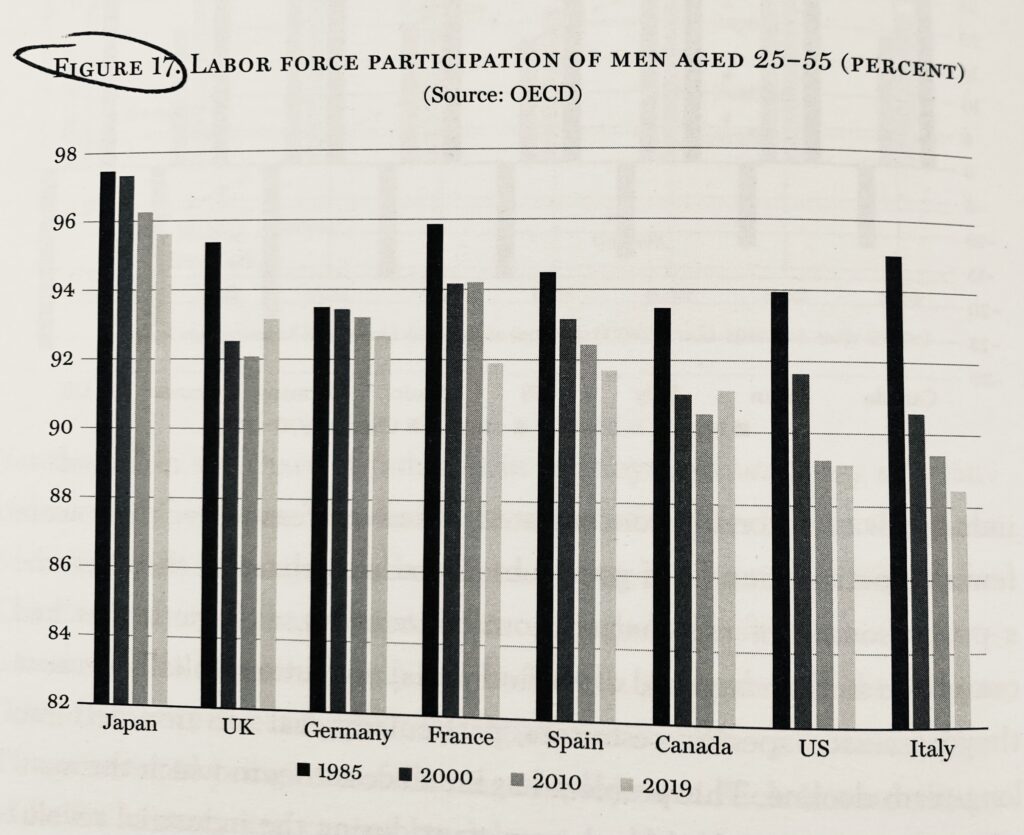

The most striking fact about labour markets over recent years is the decline in labour force participation across the developed world:

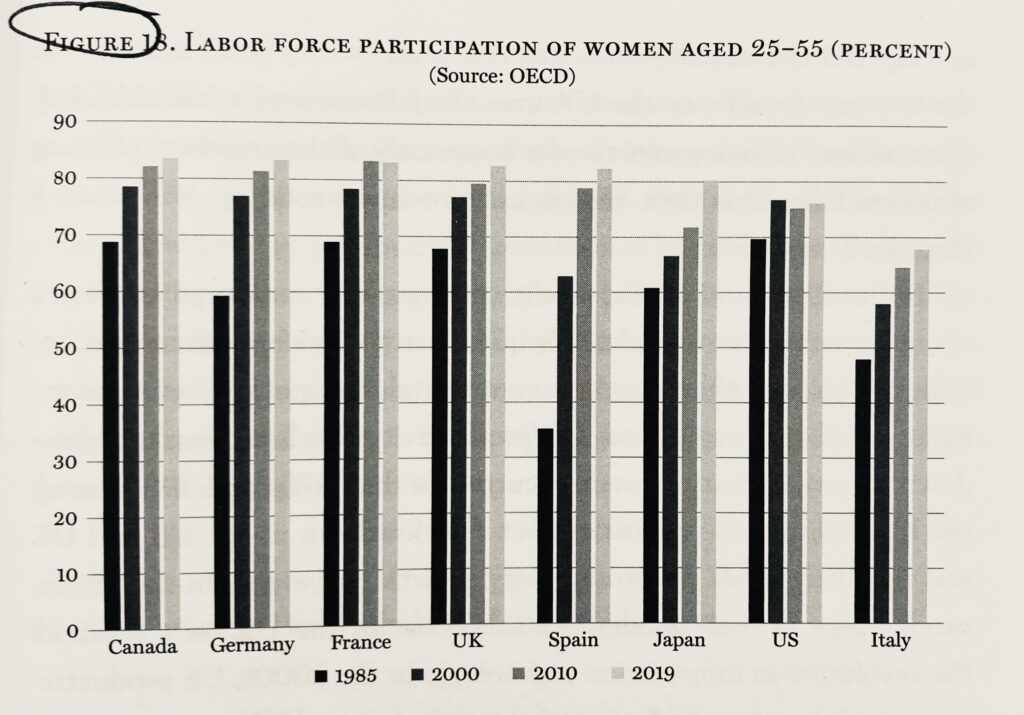

By contrast, labour force participation of women has increased:

Martin Wolf believes this is due to the following main factors:

Declining fertility (due to lower infant mortality and, perhaps, seat belt laws)

Lower household maintenance costs

Declining relevance of physical strength for productive activity

Rise of the service economy

But notice how, in the US, the prime-age female participation rate has in fact fallen from 2000 to 2019. These images are from: Wolf, M., 2023, The crisis of democratic capitalism, Allen Lane, p. 96.

Learning Objectives: To understand what capital goods are

Spotlight on sustainability: Look at instances where resources have been reconfigured for alternate uses

Case: Hild, M., Dwidevy, A., and Raj, A., 2004, “The Biggest Auction Ever: 3G Licensing in Western Europe”, Darden Business Publishing

Discussion question: What are the alternatives to auctions?

Textbook Reading: Chapter 3 (Intro and Section 3.3; pp. 65-67 and pp.83-89) and Chapter 12 (Section 12.4; pp. 434-437

In this lecture video Tim Roughgarden “provides a detailed case study of the 2016-2017 Federal Communications Commission incentive auction for repurposing wireless spectrum”. It demonstrates how economics, computer science and business can coincide to solve complete real world problems. For a short overview of the success of spectrum auctions, see here:

Instructor resource: The Biggest Auction Ever: What Happened Next?, February 2019 +

You can test you knowledge of this session with this quiz.

This video introduces two key concepts: the Coase theorem, and the transitional gains trap.

In the past I have used an assignment where I asked students to link together the concepts from the video with the 3G license auction. Here is a great example of their work:

Learning Objectives: To consider how auctions compare to other allocation mechanisms. To understand different types of auction and apply them to real examples.

Cutting edge theory: Auctions are used in e-commerce

Focus on diversity: An expert on applied auction formats, Susan Athey was the first female winner of the John Bates Clark medal. She has been an advisor to Microsoft and you can follow her on Twitter here.

Spotlight on sustainability: How governments can use beauty contests to mitigate the environmental impact of infrastructure spending

“If the opportunity existed so that I could help out someone in need while helping myself, I might do it,” Bellocchio said.

Bellocchio argues that kidney transplants are low-risk procedures, and notes that you can donate an organ — even though you can’t sell one.

“Altruistic donors are lauded for their selflessness. Their vital role in saving lives is undeniable,” the court papers say.

“However, demand outstrips supply, and there is no valid constitutional or public policy rationale why one should not be able to receive a profit from such a transaction.”

The issue of repugnance rests on the claim that the moral status of an activity shouldn’t hinge on whether money changes hands. If something is morally permissible to exchange for free, then people should be allowed to trade. Another way of thinking about this is that the reason slavery was wrong was because of the slavery, not the profits. If someone “donated” a slave, that wouldn’t be ok.

Common rejoinders to markets include things like:

Financial compensation commodities the good/service and thus changes our relationship with it. As Peter Jaworski explains in the podcast linked below, we buy and sell dogs and that doesn’t mean we treat them as mere objects.

Consider the case of sulphur dioxide emissions (via McMillan, J., (2002) Reinventing the Bazaar, W.W. Norton & Co. (p.182-187) link), and notice how for many environmental activists the moral objections to trading rights to pollute seemingly outweighed the dramatic progress on reducing harmful pollution. This implies that switching people’s mindset to tolerate market mechanisms could be an incredibly powerful tool to improve the world around us.

The Story of Vaccine CA is a really good example of an urgent allocation problem that cannot be solved by markets or by central planning. It’s an ethnographic and anecdotal account of a 200 day period where tech volunteers got together to alert American’s on where covid shots were available.

Listen:

Ep. 2, Peter Jaworski – Should Markets Have Limits? The Curious Task, August 14th 2019 – in this interview Peter Jaworski argues that If it’s morally permissible to donate blood plasma it should be ok to be paid for it. In fact, if we pay companies for plasma bought from Americans, why not pay Canadians? And if every other person involved (doctors, nurses, equipment suppliers, logistics) is being paid, why shouldn’t the person making the donation?

Learning Objectives: Understand the scope and ethical boundaries of markets

Focus on diversity: Virginia Postrel’s decision to donate a kidney, and write about it, provides a personal and inspirational view of the topic.